Indexed Universal Life or IUL simplified :

IUL’s combines the protection features of Life Insurance and potential Cash Value Appreciation in one product. There are various options for Cash Value Appreciation using growth tied to market indexes or a fixed declared rate.

The premium paid is allocated for Life Insurance coverage, fees for Investment management and then the rest is allocated towards Investments. Due to the growth potential of premiums paid, sales of these policies are on a hot streak.

How does it differ from a Term Life Insurance Policy ?

A Term Life Policy is for a fixed period although it can be extended. An Indexed Universal Life Policy is a Whole life Policy that has Insurance and Savings. The Savings component can be invested in a market tracking index or into a fixed rate of interest instrument. Since there is no Savings component in a Term Life Policy, it is cheaper than IUL.

Who is this policy primarily for?

The ideal client for an IUL is someone who is considering a whole life policy, wants higher returns than a CD but does not want to participate in the stock market, maxed out 401k, Roth and is looking for tax deferred growth along with Insurance coverage.

Isn’t this a product associated with High fees ?

Let’s breakdown the fee structure for an IUL. The Policy premium is used for Insurance costs, Any rider charges, administrative costs and Investment costs.

Depending on Age/Sex/Health Status/Coverage, the costs can be as vary between 50% on the higher side to 20% on the lower side of the first year premium. The surrender value(money that you can take out of the policy and end it) of an IUL almost never reaches the invested amount in the first 6-8 years, depending on the indexes chosen. These charges vary between Insurance carriers so it’s best to compare between different Insurance companies and look at the cost section of the Illustration.

If you need help with this analysis, please reach out to us for an unbiased comparison. Contact us.

What are the investment choices in an IUL?

Let’s not call it an Investment, this is more like a Savings. In fact even the Insurance companies note that the returns are Interest and not Cap Gains or Dividends.

Choices offered vary by Insurance companies, but most of them can be grouped into Guaranteed returns and Non-Guaranteed returns.

Guaranteed returns are vey minimal and if this is selected, the policy will most like lapse in the later years.

Non-Guaranteed returns – This is the primary reason for selecting an IUL vs a whole life policy. You can choose different Indexes tied to Nasdaq-100, S&P 500, a blend of multiple indexes, Global indexes, Commodity indexes like Oil/Gold. Allocation of premium to different indexes can be done with the help of your agent or on your own if the Insurance company allows it. Here is a sample of Indexes from Nationwide –

1-Yr Multi-Index

1-Yr S&P 500

1-Yr Uncapped S&P 500

1-Yr High-Cap Multi-Index

1-Yr High-Cap S&P 500

1-Yr JPM Mercury Plus*

1-Yr BNPP Global H-Factor Plus*

1-Yr JPM Mercury

1-Yr BNPP Global H-Factor

1-Yr JPM Mercury

1-Yr BNPP Global H-Factor

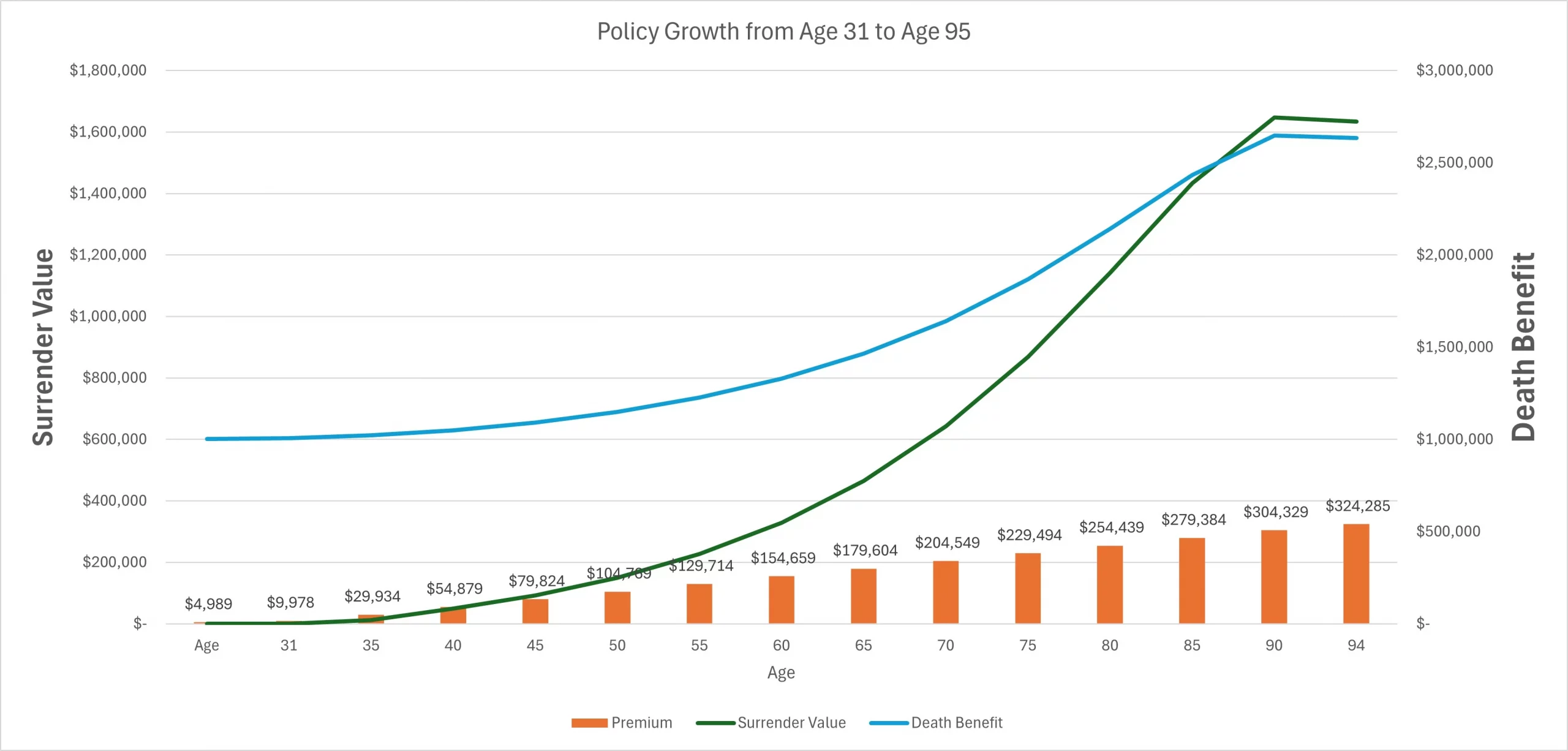

What would be a typical return scenario for a 30 yr old Female, non-smoker living in Louisville, KY in Preferred Plus category?

Assuming the policy is for a face value of $1 million with increasing death benefit and Non-Mec, selected the 1-Yr S&P 500 with an illustrated return rate of 6.47%, the annual premium is about $5,000. This is the growth of the policy, after all costs –

The Policy values catch up to the cumulative premium paid after about 8 years and then reach a high of $1 million by Age 80. Note that even though this is tracking the S&P 500, it uses a low rate of 6.47% growth. In the years the S&P 500 turns negative, the IUL will not lose value. Death benefit also grows substantially to $2+ million by Age 80.

These values will definitely change from the 6.47%.

What are the pros/cons of an IUL?

Like every Insurance product, an IUL also has it’s share of Pros and Cons.

Pros –

- IUL offers whole life coverage with a possibility of substantial returns on premium paid. This depends on the selected Index performance.

- Flexibility of paying premiums as in Monthly, Quarterly, Semi-Annually or Annual. Some carriers also permit Single Premium or paying higher amounts during the early years of the policy.

- Various Index choices and option to select fixed interest rate option also.

- No direct participation in the markets, so Policy values do not fluctuate on a daily basis.

- 0% Floor rate prevents Policy value from decreasing even if Index selected turns negative.

- Option to take a loan and not affect Death Benefit.

- Interest compounds every year of positive Index years and grows tax deferred.

Cons –

- IUL is a complicated product to understand unlike Whole life or Term Insurance.

- Improper Index selection can degrade performance.

- Insurance companies can alter the Cap rate and/or Par rate depending on the Interest rate environment and market volatility. This will affect performance.

- In the Initial years of the policy, Living Benefits will be substantially lower.

- Policy can lapse if Index performance for the first few years is not positive.

- Higher costs compared to Term Policies.

What is max funding an IUL?

As you have seen above, IUL’s start gaining over the premium paid only after a few years. If the IUL does not grow due to Indexes being at zero for a few years, then there is a risk that the policy may not have sufficient value to cover premiums at a later age. To avoid this, the following is suggested –

- Select the Policy as a non-Mec, this option will allow for tax free loans.

- Use the Increasing Death benefit option.

- If possible front load the policy with the highest premium the policy will allow with being a MEC status. You can also use a single premium or 7 pay to front load the policy.

- Select a market participation index and not the guaranteed index.